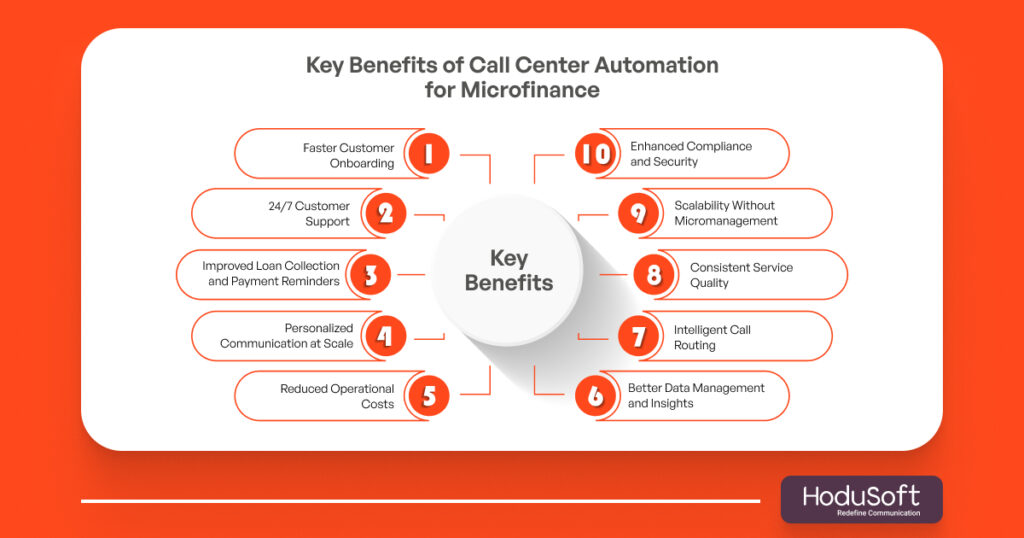

Call center automation doesn’t just optimize existing processes—it completely transforms how microfinance institutions engage with borrowers. Here’s how it plays a pivotal role in scaling:

1. Faster Customer Onboarding

Call center automation makes onboarding new borrowers quicker and more efficient. Automated IVR systems and chatbots can collect essential documents, verify KYC details, and guide clients through the loan application process without needing human intervention at every step. This helps microfinance companies serve more clients without overwhelming their teams.

2. 24/7 Customer Support

Unlike traditional call centers that operate only during office hours, automated systems can support clients round the clock. Borrowers can get answers to common questions, check loan statuses, or request services anytime they want. This constant availability builds trust and improves the borrower experience significantly.

3. Improved Loan Collection and Payment Reminders

Automation enables microfinance companies to send timely payment reminders through calls, SMS, or WhatsApp messages. These reminders are consistent and personalized based on each borrower’s due dates. As a result, repayment rates improve and the number of defaults goes down without burdening human agents.

4. Personalized Communication at Scale

Even when dealing with thousands of customers, automation allows microfinance institutions to send personalized messages. Whether it’s loan approval updates, payment alerts, or service notifications, borrowers feel recognized and valued when communication feels tailored to them.

5. Reduced Operational Costs

Hiring and training call center agents for every stage of the customer journey is expensive. Automated systems can handle repetitive tasks like FAQs, appointment scheduling, and reminders, allowing human agents to focus only on complex queries. This brings down operational costs without sacrificing service quality.

6. Better Data Management and Insights

Automation platforms can track every interaction, store important borrower information, and generate reports. This helps microfinance companies monitor trends, understand borrower behavior, and make data-driven decisions to improve services and lending strategies.

7. Intelligent Call Routing

When a borrower needs specialized assistance, automated systems can route the call to the right department or agent based on predefined rules. This ensures that clients don’t have to explain their issues multiple times or get bounced between different people, improving customer satisfaction.

8. Consistent Service Quality

Human agents may sometimes have off days, but automated systems provide consistent service every time. Standardized scripts, response templates, and process flows ensure that all borrowers receive accurate, uniform information no matter when they call.

9. Scalability Without Micromanagement

As microfinance companies grow, manual customer service becomes harder to manage. Call center automation allows businesses to scale operations effortlessly, handling larger volumes of interactions without needing to hire and micromanage large teams.

10. Enhanced Compliance and Security

Automated systems can be programmed to follow regulatory guidelines during every interaction. From data privacy to audit trails, automation helps microfinance companies stay compliant while reducing the risk of human errors that could lead to penalties.

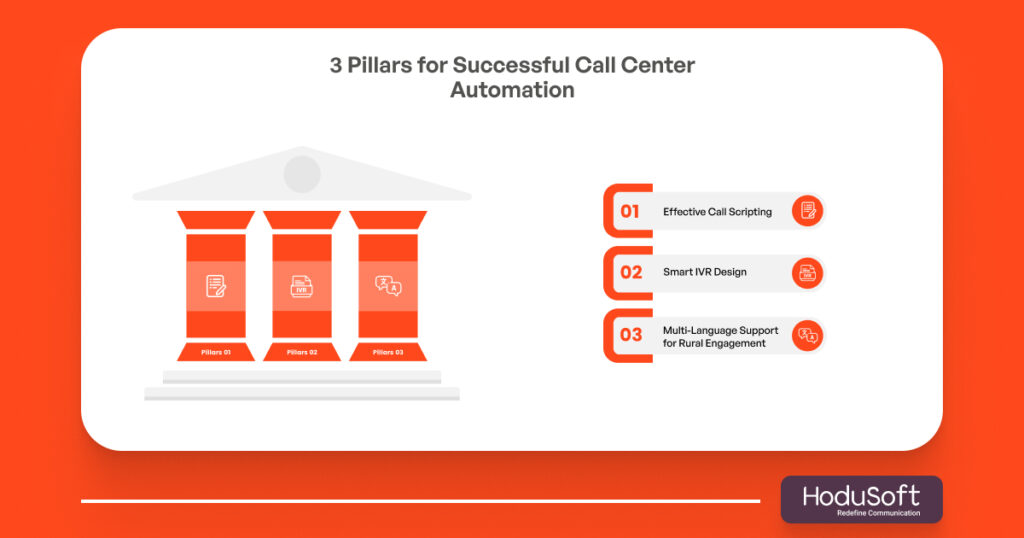

To truly unlock the power of automation in scaling lending, microfinance institutions must focus on these three critical pillars:

1. Effective Call Scripting

Scripts must be clear, friendly, and easy to understand, especially for borrowers who may be unfamiliar with financial jargon.

Scripts should cover key scenarios: loan application updates, repayment reminders, payment confirmations, grievance handling, and loan closure.

They should sound natural, not robotic, guiding both live agents and voicebots toward positive borrower experiences.

2. Smart IVR Design

An IVR system is often the borrower’s first interaction with the lender — it must be intuitive.

Simple, action-oriented options like “Press 1 for your next payment date,” “Press 2 for loan status,” and “Press 3 to connect with an agent” help borrowers navigate quickly without frustration.

Customizing IVR flows based on language, loan type, or account status can further enhance borrower engagement and reduce drop-offs.

3. Multi-Language Support for Rural Engagement

Supporting multiple languages—not just major ones such as English or French but regional dialects—is vital for connecting with rural borrowers.

Voicebots, IVR prompts, SMS reminders, and WhatsApp messages should all be localized, using simple words and culturally appropriate messaging to build trust and drive action.